At Shara, our mission is to fill a significant gap in financial services for small businesses and everyday consumers in Africa. The current banking system heavily favors high-end corporations and wealthy individuals, leaving the majority burdened with high fees and complex credit requirements. Shara is changing this by providing seamless, fee-free transactions and embedded financing solutions tailored to the needs of SMEs and consumers.

Shara

Overview

Shara offers financing to Small and Medium Enterprises (SMEs) across Africa. With our scoring model and favorable credit terms, we have built a user base of over 5,000 merchants who rely on replenishing credit lines every month to sustain and grow their businesses.

Our journey began with market visits around Nairobi. We observed that many fintech solutions were exploitative and disconnected from the realities of our customers. From years of research and data collected by Shara employees, we discovered that people in these communities rarely default on each other. Trust within these networks is strong, forming the backbone of consumer credit in emerging markets, where SMEs often finance their best customers—friends and family.

My Role: Product Designer, Research, Branding & Marketing

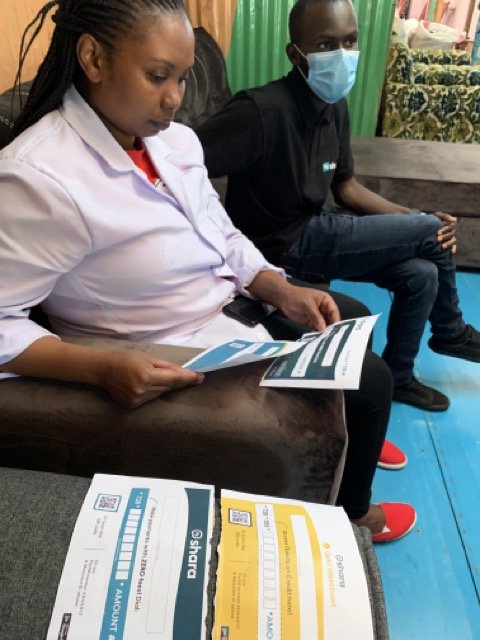

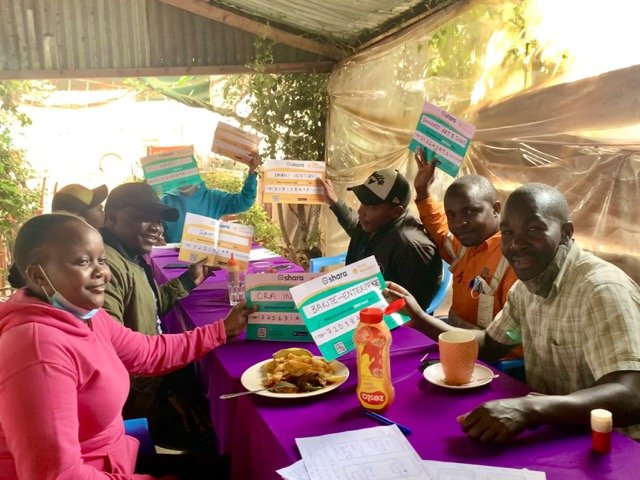

I played a key role in the testing and development of loan repayment flows, as well as in researching, branding, and marketing for Shara. A significant part of my work involved capturing the essence of community-driven finance, on and offline. One of my favorite projects was driving the move away from generic stock images that failed to convey our message and instead, I ventured into the streets of Gachie with a photographer. Together, we documented the real connections between merchants and their customers, deepening our understanding of the market's credit relationshinships and business needs. These images are now a core element of Shara’s branding materials. (Photo, Left)

Identifying the Problem

Existing financial institutions, including banks and fintech products, do not adequately serve SMEs or the average consumer. Credit is both expensive and difficult to obtain, with banks imposing high interest rates and stringent collateral requirements. This leaves a significant gap in the market for SME and consumer credit. SMEs often use their own stock capital to finance trusted clients, limiting their growth potential. Additionally, there is a lack of creative financial tools that align with the way business is conducted in these markets. Trust in financial products beyond close-knit networks is low, further restricting access to credit.

Research

To understand our users better, we developed personas representing SME owners and consumers. These helped us pinpoint specific needs and challenges.

We spent considerable time in the field, distributing brochures to test our value proposition and validate product offerings before diving into product development.

Prototyping

Using high-fidelity prototypes created in Figma and linked to Android devices, we observed merchant interactions. This process highlighted areas for improvement and clarity before the engineering team began development on our initial concepts.

Nairobi’s markets provided a rich source of real-time customer feedback and insights. These in-person conversations with users in their daily business environments were invaluable, offering a depth of understanding that phone calls or customer support meetings couldn't match.

Persona Development

To gain a deeper understanding of our target audience, we developed detailed personas representing typical SME owners and consumers who rely on community trust for their financial transactions. For instance, a hardware store owner extends credit to regular customers based on personal relationships, while a consumer prefers shopping at trusted local stores where they can negotiate payment terms.

Ecosytem research

Our analysis of the financial ecosystem revealed that SMEs and consumers operate within a fragmented and inefficient system. SMEs often finance their trusted clients using their own resources, limiting their growth potential. There is a clear need for financial tools that align with how business is conducted in these markets and leverage existing trust networks to facilitate credit and transactions.

Experimentation

We tested various products to understand what worked best for our users. Distributing flyers helped validate our hypotheses. One such hypothesis was the development of a consumer app for credit transactions. However, merchants were uncomfortable with this approach, preferring to maintain control over their finances privately. This feedback led us to halt further development of the consumer app.

Merchants valued being in control of their finances and managing their credit cycles privately. While they appreciated prompt reminders and responsive customer support, they were not ready to involve their customers in their credit journey.

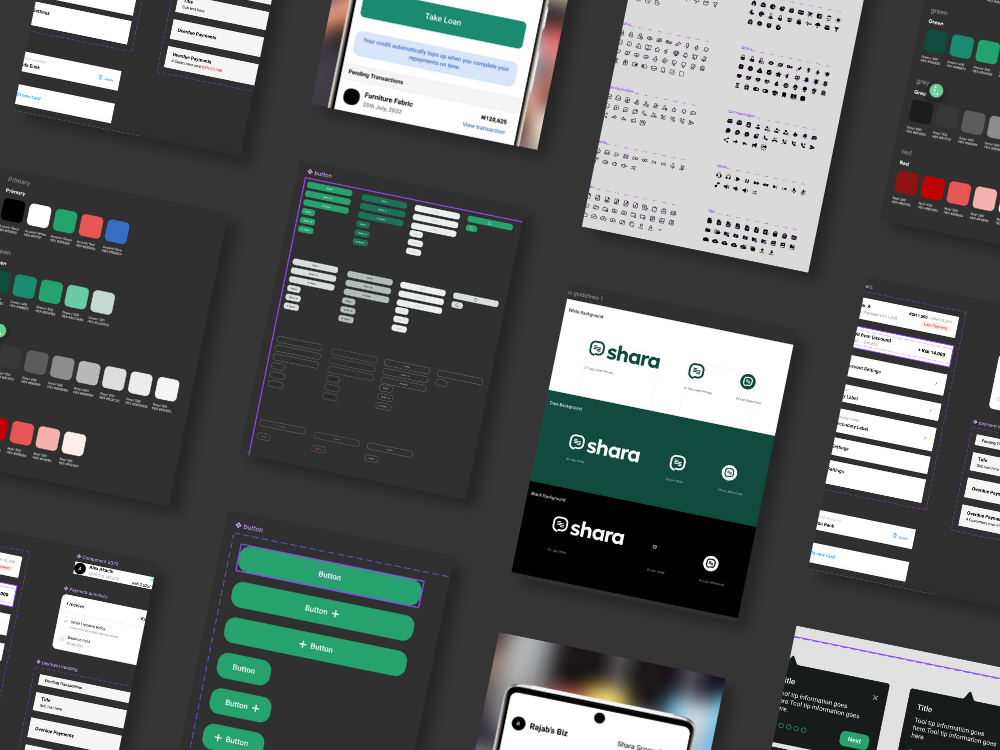

Design & documentation

Continuous experimentation allowed us to refine both our product offerings and design language. We built on Shara’s reputation as a reliable financing solution with stellar customer support and innovative credit offerings. Key design decisions included:

Brand Identity:

Color Palette: We chose a modern, approachable color scheme that conveys trust and reliability. Soft greens, white and black to represent financial stability and growth.

Typography: Clean, sans-serif fonts were selected for readability and to convey a sense of modernity and professionalism.

User Experience (UX):

Seamless Onboarding: Streamlined to allow users to open an account quickly with minimal steps. Digital KYC (Know Your Customer) processes were implemented to facilitate this.

Personalized Dashboards: Tailored based on user type (e.g., SME owner, consumer) to ensure relevant information and tools are readily available.

Integrated Support: Customer support features, such as live chat and a comprehensive help center, were embedded within the app, ensuring users can easily get assistance when needed.

Community Leads: All Shara merchants were assigned a customer support rep or Community lead who could visit their shop and help troubleshoot when needed.

Visual and Interaction Design:

Micro-Interactions: Small, thoughtful animations and interactions were added to enhance user engagement and provide feedback, making the app feel more responsive and intuitive.

Iconography: Custom icons were designed to be clear and universally understandable, supporting users with varying levels of literacy and tech-savviness.

Responsive Design: The platform was designed to be fully responsive, ensuring a seamless experience across different devices and screen sizes.

Community Engagement:

User Stories and Testimonials: Real user stories and testimonials were incorporated within the app and marketing materials to build credibility and connect with potential users on a personal level.

Feedback Loops: Regular feedback sessions and usability tests were conducted with users to continuously gather insights and iterate on the design, ensuring the product evolves with user needs.

Testing & iteration

We conducted extensive testing with a beta cohort of users, including hardware stores, furniture makers, and FMCG distributors. This testing phase was crucial for refining our product and ensuring it met the needs of our target users.

Key milestones in our testing and iteration process included:

Initial Launch: Introducing Shara to a select group of SMEs to gather initial feedback.

User Feedback: Collecting and analyzing feedback from both SMEs and consumers to identify areas for improvement.

Platform Refinement: Iterating on our design based on user feedback, focusing on enhancing usability and functionality.

Summary

Shara is redefining community finance for the digital age by building a platform that leverages social trust networks and provides embedded financial tools. By understanding the unique needs of SMEs and consumers in emerging markets, Shara offers a solution that aligns with existing business practices, fostering trust and financial inclusion. Our design process, grounded in extensive research and user feedback, ensures that Shara provides real value to its users, creating a sustainable and community-driven financial ecosystem.